Spatial simultaneous autoregressive error model estimation by GMM

GMerrorsar.RdAn implementation of Kelejian and Prucha's generalised moments estimator for the autoregressive parameter in a spatial model.

Usage

GMerrorsar(formula, data = list(), listw, na.action = na.fail,

zero.policy = attr(listw, "zero.policy"), method="nlminb", arnoldWied=FALSE,

control = list(), pars, scaleU=FALSE, verbose=NULL, legacy=FALSE,

se.lambda=TRUE, returnHcov=FALSE, pWOrder=250, tol.Hcov=1.0e-10)

# S3 method for class 'Gmsar'

summary(object, correlation = FALSE, Hausman=FALSE, ...)

GMargminImage(obj, lambdaseq, s2seq)Arguments

- formula

a symbolic description of the model to be fit. The details of model specification are given for

lm()- data

an optional data frame containing the variables in the model. By default the variables are taken from the environment which the function is called.

- listw

a

listwobject created for example bynb2listw- na.action

a function (default

na.fail), can also bena.omitorna.excludewith consequences for residuals and fitted values - in these cases the weights list will be subsetted to remove NAs in the data. It may be necessary to set zero.policy to TRUE because this subsetting may create no-neighbour observations. Note that only weights lists created without using the glist argument tonb2listwmay be subsetted.- zero.policy

default NULL, use global option value; if TRUE assign zero to the lagged value of zones without neighbours, if FALSE (default) assign NA - causing

GMerrorsar()to terminate with an error- method

default

"nlminb", or optionally a method passed tooptimto use an alternative optimizer- arnoldWied

default FALSE

- control

A list of control parameters. See details in

optimornlminb.- pars

starting values for \(\lambda\) and \(\sigma^2\) for GMM optimisation, if missing (default), approximated from initial OLS model as the autocorrelation coefficient corrected for weights style and model sigma squared

- scaleU

Default FALSE: scale the OLS residuals before computing the moment matrices; only used if the

parsargument is missing- verbose

default NULL, use global option value; if TRUE, reports function values during optimization.

- legacy

default FALSE - compute using the unfiltered values of the response and right hand side variables; if TRUE - compute the fitted value and residuals from the spatially filtered model using the spatial error parameter

- se.lambda

default TRUE, use the analytical method described in http://econweb.umd.edu/~prucha/STATPROG/OLS/desols.pdf

- returnHcov

default FALSE, return the Vo matrix for a spatial Hausman test

- tol.Hcov

the tolerance for computing the Vo matrix (default=1.0e-10)

- pWOrder

default 250, if returnHcov=TRUE, pass this order to

powerWeightsas the power series maximum limit- object, obj

Gmsarobject fromGMerrorsar- correlation

logical; (default=FALSE), TRUE not available

- Hausman

if TRUE, the results of the Hausman test for error models are reported

- ...

summaryarguments passed through- lambdaseq

if given, an increasing sequence of lambda values for gridding

- s2seq

if given, an increasing sequence of sigma squared values for gridding

Details

When the control list is set with care, the function will converge to values close to the ML estimator without requiring computation of the Jacobian, the most resource-intensive part of ML estimation.

Note that the fitted() function for the output object assumes that the response variable may be reconstructed as the sum of the trend, the signal, and the noise (residuals). Since the values of the response variable are known, their spatial lags are used to calculate signal components (Cressie 1993, p. 564). This differs from other software, including GeoDa, which does not use knowledge of the response variable in making predictions for the fitting data.

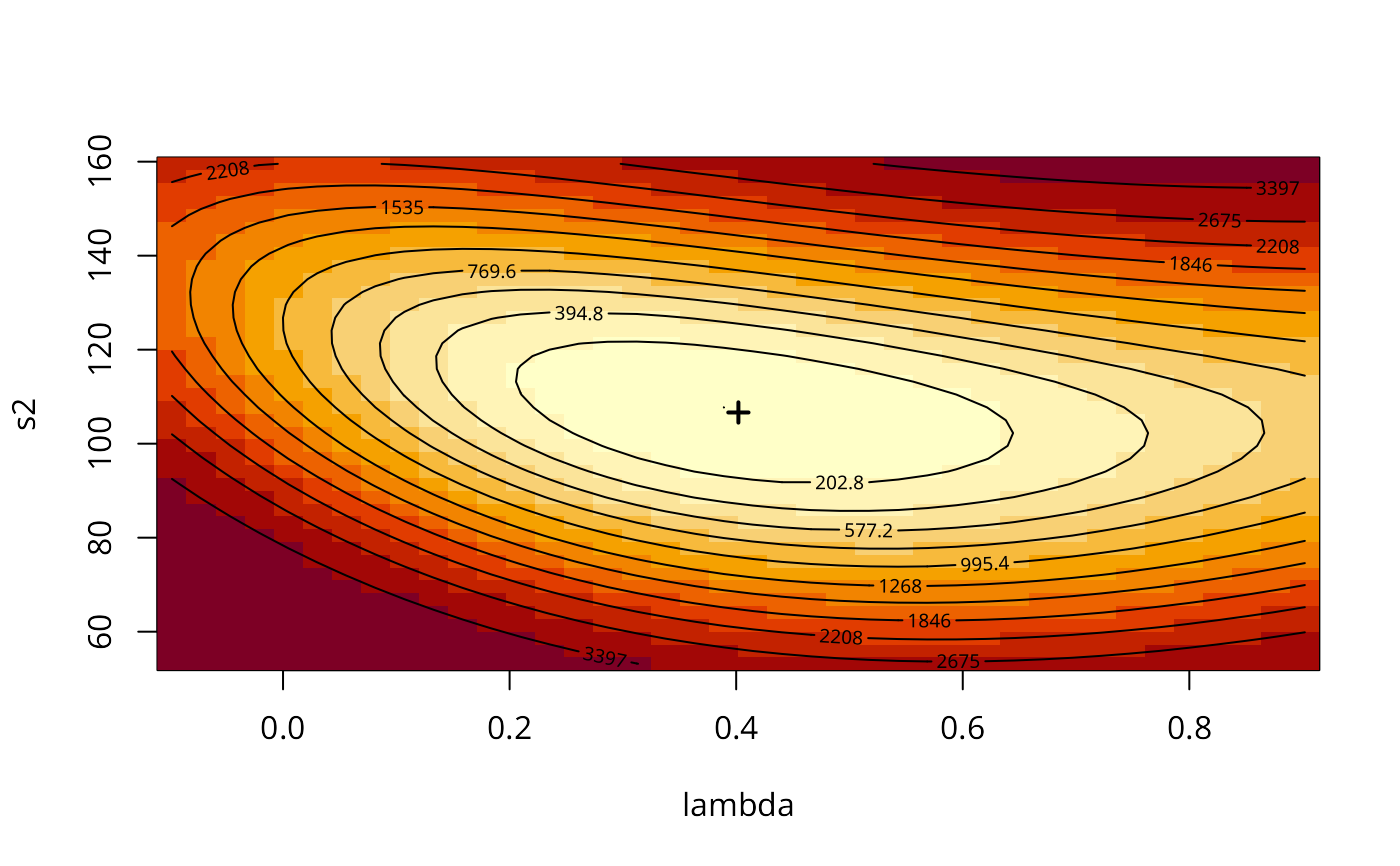

The GMargminImage may be used to visualize the shape of the surface of the argmin function used to find lambda.

Value

A list object of class Gmsar

- type

"ERROR"

- lambda

simultaneous autoregressive error coefficient

- coefficients

GMM coefficient estimates

- rest.se

GMM coefficient standard errors

- s2

GMM residual variance

- SSE

sum of squared GMM errors

- parameters

number of parameters estimated

- lm.model

the

lmobject returned when estimating for \(\lambda=0\)- call

the call used to create this object

- residuals

GMM residuals

- lm.target

the

lmobject returned for the GMM fit- fitted.values

Difference between residuals and response variable

- formula

model formula

- aliased

if not NULL, details of aliased variables

- zero.policy

zero.policy for this model

- vv

list of internal bigG and litg components for testing optimisation surface

- optres

object returned by optimizer

- pars

start parameter values for optimisation

- Hcov

Spatial DGP covariance matrix for Hausman test if available

- legacy

input choice of unfiltered or filtered values

- lambda.se

value computed if input argument TRUE

- arnoldWied

were Arnold-Wied moments used

- GMs2

GM argmin sigma squared

- scaleU

input choice of scaled OLS residuals

- vcov

variance-covariance matrix of regression coefficients

- na.action

(possibly) named vector of excluded or omitted observations if non-default na.action argument used

References

Kelejian, H. H., and Prucha, I. R., 1999. A Generalized Moments Estimator for the Autoregressive Parameter in a Spatial Model. International Economic Review, 40, pp. 509–533; Cressie, N. A. C. 1993 Statistics for spatial data, Wiley, New York.

Roger Bivand, Gianfranco Piras (2015). Comparing Implementations of Estimation Methods for Spatial Econometrics. Journal of Statistical Software, 63(18), 1-36. doi:10.18637/jss.v063.i18 .

Examples

#require("spdep", quietly=TRUE)

data(oldcol, package="spdep")

COL.errW.eig <- errorsarlm(CRIME ~ INC + HOVAL, data=COL.OLD,

spdep::nb2listw(COL.nb, style="W"), method="eigen")

(x <- summary(COL.errW.eig, Hausman=TRUE))

#>

#> Call:

#> errorsarlm(formula = CRIME ~ INC + HOVAL, data = COL.OLD, listw = spdep::nb2listw(COL.nb,

#> style = "W"), method = "eigen")

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -34.81174 -6.44031 -0.72142 7.61476 23.33626

#>

#> Type: error

#> Coefficients: (asymptotic standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 59.893219 5.366163 11.1613 < 2.2e-16

#> INC -0.941312 0.330569 -2.8476 0.0044057

#> HOVAL -0.302250 0.090476 -3.3407 0.0008358

#>

#> Lambda: 0.56179, LR test value: 7.9935, p-value: 0.0046945

#> Asymptotic standard error: 0.13387

#> z-value: 4.1966, p-value: 2.7098e-05

#> Wald statistic: 17.611, p-value: 2.7098e-05

#>

#> Log likelihood: -183.3805 for error model

#> ML residual variance (sigma squared): 95.575, (sigma: 9.7762)

#> Number of observations: 49

#> Number of parameters estimated: 5

#> AIC: 376.76, (AIC for lm: 382.75)

#> Hausman test: 4.902, df: 3, p-value: 0.17911

#>

coef(x)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 59.8932192 5.36616252 11.161276 0.0000000000

#> INC -0.9413120 0.33056857 -2.847554 0.0044056569

#> HOVAL -0.3022502 0.09047605 -3.340665 0.0008357788

COL.errW.GM <- GMerrorsar(CRIME ~ INC + HOVAL, data=COL.OLD,

spdep::nb2listw(COL.nb, style="W"), returnHcov=TRUE)

(x <- summary(COL.errW.GM, Hausman=TRUE))

#>

#> Call:

#> GMerrorsar(formula = CRIME ~ INC + HOVAL, data = COL.OLD, listw = spdep::nb2listw(COL.nb,

#> style = "W"), returnHcov = TRUE)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -30.5432 -6.5553 -2.1921 10.0553 28.7497

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 62.513752 5.121339 12.207 < 2.2e-16

#> INC -1.128283 0.339745 -3.321 0.000897

#> HOVAL -0.296957 0.095699 -3.103 0.001915

#>

#> Lambda: 0.40196 (standard error): 0.42334 (z-value): 0.94948

#> Residual variance (sigma squared): 106.64, (sigma: 10.327)

#> GM argmin sigma squared: 106.36

#> Number of observations: 49

#> Number of parameters estimated: 5

#> Hausman test: 6.6406, df: 3, p-value: 0.08428

#>

coef(x)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 62.5137525 5.12133863 12.206526 0.0000000000

#> INC -1.1282834 0.33974492 -3.320972 0.0008970455

#> HOVAL -0.2969573 0.09569889 -3.103038 0.0019154486

aa <- GMargminImage(COL.errW.GM)

levs <- quantile(aa$z, seq(0, 1, 1/12))

image(aa, breaks=levs, xlab="lambda", ylab="s2")

points(COL.errW.GM$lambda, COL.errW.GM$s2, pch=3, lwd=2)

contour(aa, levels=signif(levs, 4), add=TRUE)

COL.errW.GM1 <- GMerrorsar(CRIME ~ INC + HOVAL, data=COL.OLD,

spdep::nb2listw(COL.nb, style="W"))

summary(COL.errW.GM1)

#>

#> Call:

#> GMerrorsar(formula = CRIME ~ INC + HOVAL, data = COL.OLD, listw = spdep::nb2listw(COL.nb,

#> style = "W"))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -30.5432 -6.5553 -2.1921 10.0553 28.7497

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 62.513752 5.121339 12.207 < 2.2e-16

#> INC -1.128283 0.339745 -3.321 0.000897

#> HOVAL -0.296957 0.095699 -3.103 0.001915

#>

#> Lambda: 0.40196 (standard error): 0.42334 (z-value): 0.94948

#> Residual variance (sigma squared): 106.64, (sigma: 10.327)

#> GM argmin sigma squared: 106.36

#> Number of observations: 49

#> Number of parameters estimated: 5

#>

require("sf", quietly=TRUE)

nydata <- st_read(system.file("shapes/NY8_bna_utm18.gpkg", package="spData")[1], quiet=TRUE)

suppressMessages(nyadjmat <- as.matrix(foreign::read.dbf(system.file(

"misc/nyadjwts.dbf", package="spData")[1])[-1]))

suppressMessages(ID <- as.character(names(foreign::read.dbf(system.file(

"misc/nyadjwts.dbf", package="spData")[1]))[-1]))

identical(substring(ID, 2, 10), substring(as.character(nydata$AREAKEY), 2, 10))

#> [1] TRUE

listw_NY <- spdep::mat2listw(nyadjmat, as.character(nydata$AREAKEY), style="B")

esar1f <- spautolm(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME, data=nydata,

listw=listw_NY, family="SAR", method="eigen")

summary(esar1f)

#>

#> Call:

#> spautolm(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME, data = nydata,

#> listw = listw_NY, family = "SAR", method = "eigen")

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.56754 -0.38239 -0.02643 0.33109 4.01219

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.618193 0.176784 -3.4969 0.0004707

#> PEXPOSURE 0.071014 0.042051 1.6888 0.0912635

#> PCTAGE65P 3.754200 0.624722 6.0094 1.862e-09

#> PCTOWNHOME -0.419890 0.191329 -2.1946 0.0281930

#>

#> Lambda: 0.040487 LR test value: 5.2438 p-value: 0.022026

#> Numerical Hessian standard error of lambda: 0.017197

#>

#> Log likelihood: -276.1069

#> ML residual variance (sigma squared): 0.41388, (sigma: 0.64333)

#> Number of observations: 281

#> Number of parameters estimated: 6

#> AIC: 564.21

#>

esar1gm <- GMerrorsar(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

data=nydata, listw=listw_NY)

summary(esar1gm)

#>

#> Call:GMerrorsar(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

#> data = nydata, listw = listw_NY)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.641411 -0.396370 -0.026618 0.341740 4.204264

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.604364 0.174576 -3.4619 0.0005364

#> PEXPOSURE 0.067902 0.041164 1.6496 0.0990337

#> PCTAGE65P 3.775308 0.622965 6.0602 1.359e-09

#> PCTOWNHOME -0.437545 0.188906 -2.3162 0.0205468

#>

#> Lambda: 0.03605 (standard error): 0.2022 (z-value): 0.17829

#> Residual variance (sigma squared): 0.41585, (sigma: 0.64487)

#> GM argmin sigma squared: 0.45141

#> Number of observations: 281

#> Number of parameters estimated: 6

#>

esar1gm1 <- GMerrorsar(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

data=nydata, listw=listw_NY, method="Nelder-Mead")

summary(esar1gm1)

#>

#> Call:GMerrorsar(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

#> data = nydata, listw = listw_NY, method = "Nelder-Mead")

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.641390 -0.396374 -0.026616 0.341745 4.204277

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.604384 0.174580 -3.4619 0.0005363

#> PEXPOSURE 0.067907 0.041165 1.6496 0.0990225

#> PCTAGE65P 3.775275 0.622969 6.0601 1.36e-09

#> PCTOWNHOME -0.437518 0.188910 -2.3160 0.0205572

#>

#> Lambda: 0.036057 (standard error): 0.20221 (z-value): 0.17832

#> Residual variance (sigma squared): 0.41585, (sigma: 0.64487)

#> GM argmin sigma squared: 0.45139

#> Number of observations: 281

#> Number of parameters estimated: 6

#>

COL.errW.GM1 <- GMerrorsar(CRIME ~ INC + HOVAL, data=COL.OLD,

spdep::nb2listw(COL.nb, style="W"))

summary(COL.errW.GM1)

#>

#> Call:

#> GMerrorsar(formula = CRIME ~ INC + HOVAL, data = COL.OLD, listw = spdep::nb2listw(COL.nb,

#> style = "W"))

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -30.5432 -6.5553 -2.1921 10.0553 28.7497

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 62.513752 5.121339 12.207 < 2.2e-16

#> INC -1.128283 0.339745 -3.321 0.000897

#> HOVAL -0.296957 0.095699 -3.103 0.001915

#>

#> Lambda: 0.40196 (standard error): 0.42334 (z-value): 0.94948

#> Residual variance (sigma squared): 106.64, (sigma: 10.327)

#> GM argmin sigma squared: 106.36

#> Number of observations: 49

#> Number of parameters estimated: 5

#>

require("sf", quietly=TRUE)

nydata <- st_read(system.file("shapes/NY8_bna_utm18.gpkg", package="spData")[1], quiet=TRUE)

suppressMessages(nyadjmat <- as.matrix(foreign::read.dbf(system.file(

"misc/nyadjwts.dbf", package="spData")[1])[-1]))

suppressMessages(ID <- as.character(names(foreign::read.dbf(system.file(

"misc/nyadjwts.dbf", package="spData")[1]))[-1]))

identical(substring(ID, 2, 10), substring(as.character(nydata$AREAKEY), 2, 10))

#> [1] TRUE

listw_NY <- spdep::mat2listw(nyadjmat, as.character(nydata$AREAKEY), style="B")

esar1f <- spautolm(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME, data=nydata,

listw=listw_NY, family="SAR", method="eigen")

summary(esar1f)

#>

#> Call:

#> spautolm(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME, data = nydata,

#> listw = listw_NY, family = "SAR", method = "eigen")

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.56754 -0.38239 -0.02643 0.33109 4.01219

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.618193 0.176784 -3.4969 0.0004707

#> PEXPOSURE 0.071014 0.042051 1.6888 0.0912635

#> PCTAGE65P 3.754200 0.624722 6.0094 1.862e-09

#> PCTOWNHOME -0.419890 0.191329 -2.1946 0.0281930

#>

#> Lambda: 0.040487 LR test value: 5.2438 p-value: 0.022026

#> Numerical Hessian standard error of lambda: 0.017197

#>

#> Log likelihood: -276.1069

#> ML residual variance (sigma squared): 0.41388, (sigma: 0.64333)

#> Number of observations: 281

#> Number of parameters estimated: 6

#> AIC: 564.21

#>

esar1gm <- GMerrorsar(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

data=nydata, listw=listw_NY)

summary(esar1gm)

#>

#> Call:GMerrorsar(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

#> data = nydata, listw = listw_NY)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.641411 -0.396370 -0.026618 0.341740 4.204264

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.604364 0.174576 -3.4619 0.0005364

#> PEXPOSURE 0.067902 0.041164 1.6496 0.0990337

#> PCTAGE65P 3.775308 0.622965 6.0602 1.359e-09

#> PCTOWNHOME -0.437545 0.188906 -2.3162 0.0205468

#>

#> Lambda: 0.03605 (standard error): 0.2022 (z-value): 0.17829

#> Residual variance (sigma squared): 0.41585, (sigma: 0.64487)

#> GM argmin sigma squared: 0.45141

#> Number of observations: 281

#> Number of parameters estimated: 6

#>

esar1gm1 <- GMerrorsar(Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

data=nydata, listw=listw_NY, method="Nelder-Mead")

summary(esar1gm1)

#>

#> Call:GMerrorsar(formula = Z ~ PEXPOSURE + PCTAGE65P + PCTOWNHOME,

#> data = nydata, listw = listw_NY, method = "Nelder-Mead")

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.641390 -0.396374 -0.026616 0.341745 4.204277

#>

#> Type: GM SAR estimator

#> Coefficients: (GM standard errors)

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) -0.604384 0.174580 -3.4619 0.0005363

#> PEXPOSURE 0.067907 0.041165 1.6496 0.0990225

#> PCTAGE65P 3.775275 0.622969 6.0601 1.36e-09

#> PCTOWNHOME -0.437518 0.188910 -2.3160 0.0205572

#>

#> Lambda: 0.036057 (standard error): 0.20221 (z-value): 0.17832

#> Residual variance (sigma squared): 0.41585, (sigma: 0.64487)

#> GM argmin sigma squared: 0.45139

#> Number of observations: 281

#> Number of parameters estimated: 6

#>